As cryptocurrencies like Bitcoin and Ethereum have gained prominence, central banks around the world have taken notice. But rather than embracing decentralized digital money, many are developing their own: Central Bank Digital Currencies (CBDCs).

China’s digital yuan is already being tested with millions of users. The European Central Bank is progressing with the digital euro. The Federal Reserve is exploring a digital dollar. Over 130 countries, representing 98% of global GDP, are now exploring CBDCs.

But what exactly are CBDCs? How are they different from cryptocurrencies? And what do they mean for the future of money? This guide explains everything you need to know.

What is a CBDC?

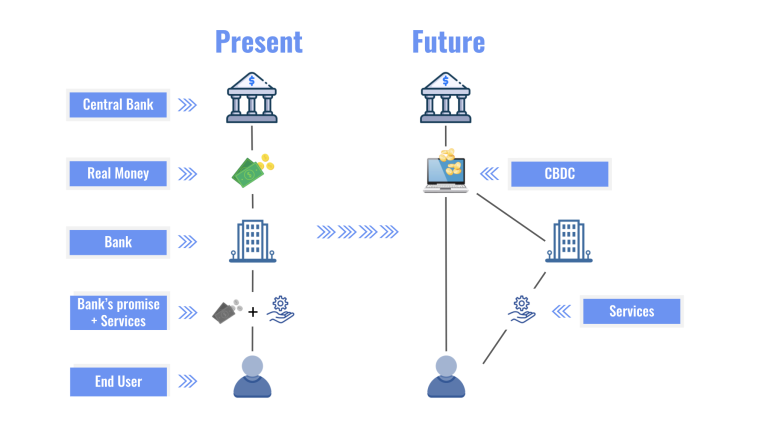

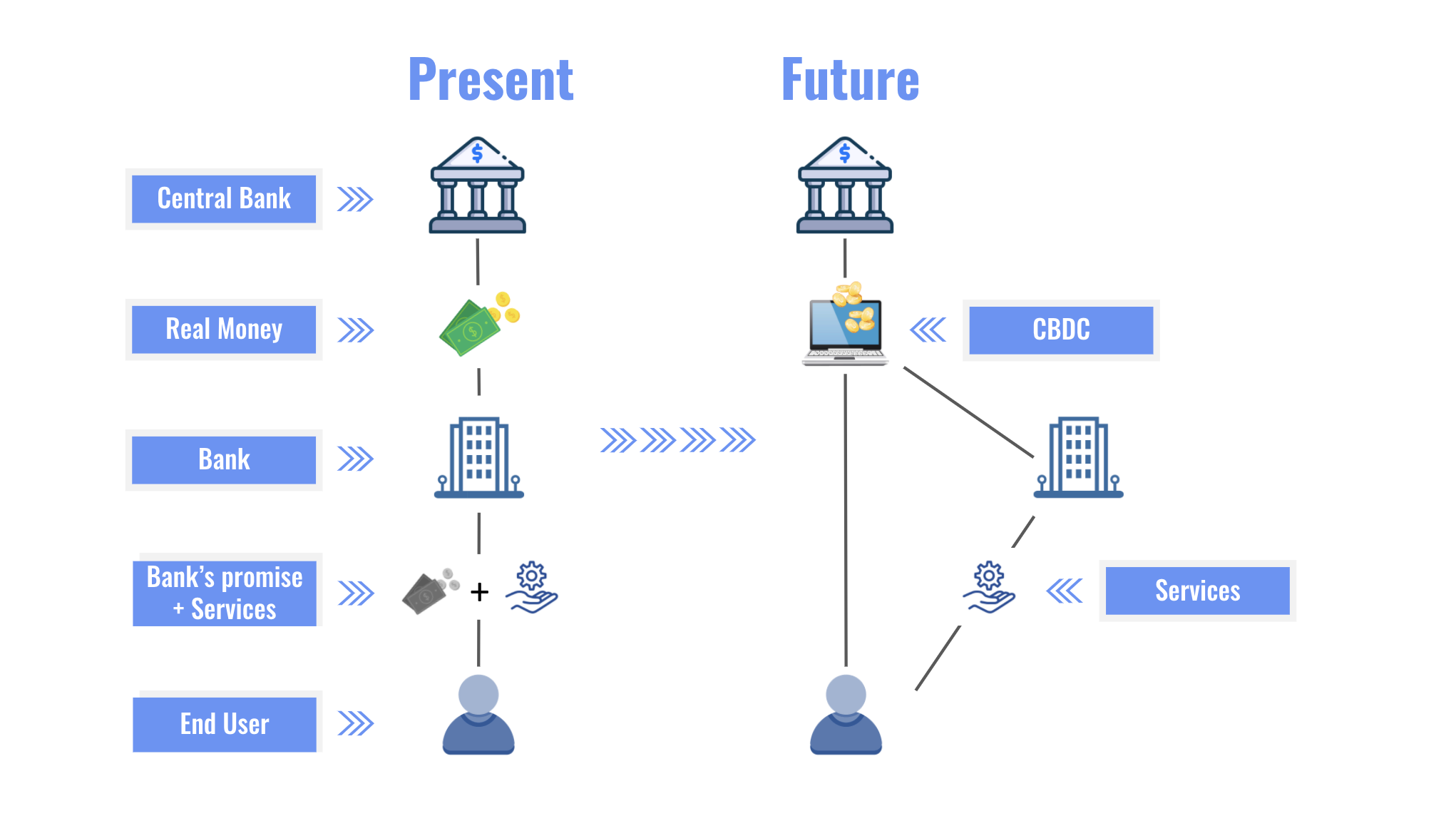

A Central Bank Digital Currency (CBDC) is a digital form of a country’s fiat currency, issued and regulated by the central bank. It’s essentially a digital version of cash—but with some important differences.

Like physical cash, a CBDC would be a liability of the central bank. Unlike commercial bank money (the digital balances in your bank account), which is a liability of the bank, CBDCs would be a direct claim on the central bank.

Think of it this way:

- Physical cash: Notes and coins, directly issued by the central bank.

- Commercial bank money: Digital balances in your bank account, backed by the bank.

- CBDC: Digital cash, directly issued by the central bank.

Why Are Central Banks Developing CBDCs?

Several factors are driving the global push toward CBDCs:

1. Declining Cash Usage

In many countries, cash use is declining. People increasingly prefer digital payments—cards, mobile apps, bank transfers. If cash disappears entirely, citizens would lose access to central bank money, relying entirely on commercial banks. CBDCs would preserve public access to risk-free central bank money in a digital world.

2. Response to Cryptocurrencies

The rise of Bitcoin, stablecoins, and decentralized finance poses a challenge to central banks’ monopoly on money. If people start using private digital currencies for payments, central banks lose control over monetary policy and financial stability. CBDCs are a way to offer a state-backed digital alternative.

3. Financial Inclusion

CBDCs could provide access to digital payments for unbanked populations. Anyone with a mobile phone could hold a CBDC wallet, without needing a traditional bank account.

4. Cross-Border Payments

International payments are currently slow and expensive. CBDCs could potentially make cross-border transactions faster and cheaper, especially if different countries’ CBDCs are interoperable.

5. Monetary Policy Tools

CBDCs could give central banks new tools. For example, they could implement “programmable money” that only works for certain purposes, or even negative interest rates by charging fees on holdings above certain limits (though this is controversial).

6. Combating Illicit Activity

While physical cash enables anonymous transactions, CBDCs could be designed with traceability, potentially helping combat money laundering, tax evasion, and terrorist financing.

How CBDCs Differ from Cryptocurrencies

Despite both being digital currencies, CBDCs and cryptocurrencies like Bitcoin are fundamentally different:

| Feature | Cryptocurrencies (Bitcoin, Ethereum) | CBDCs |

|---|---|---|

| Issuer | Decentralized, no central issuer | Central bank (government authority) |

| Control | Community-driven, decentralized | Centralized, government-controlled |

| Blockchain | Usually public, permissionless | Likely private, permissioned (or centralized database) |

| Anonymity | Pseudonymous (varies by coin) | Potentially traceable, may have limits on anonymity |

| Supply | Often fixed (Bitcoin) or algorithmic | Controlled by central bank (like fiat) |

| Purpose | Various (store of value, payments, smart contracts) | Digital version of national currency |

| Legal Tender | No (except El Salvador for Bitcoin) | Yes, by definition |

CBDC Design Choices

Not all CBDCs would work the same way. Central banks face several design decisions:

1. Retail vs. Wholesale

- Retail CBDC: Available to the general public for everyday transactions (like digital cash). Most countries are exploring this.

- Wholesale CBDC: Restricted to banks and financial institutions for interbank settlements. This is less revolutionary but could improve financial system efficiency.

2. Token-Based vs. Account-Based

- Token-based: Like physical cash or Bitcoin—if you hold the token, you own it. Transfer is like handing over a digital object.

- Account-based: Like your bank account—ownership is tied to identity, and transfers require identification.

Most CBDCs will likely be a hybrid, with some anonymity for small transactions but identity requirements for larger amounts.

3. Interest-Bearing

Could CBDCs earn interest? If yes, they might compete with bank deposits. If no, people might prefer bank accounts that do pay interest. Most early CBDCs are expected to be non-interest-bearing to avoid disrupting the banking system.

4. Programmable Money

Some envision CBDCs with “programmability”—money that can only be spent on certain things (like food stamps) or that expires after a certain time. This is highly controversial, as it gives the government unprecedented control over how you use your money.

Major CBDC Projects Around the World

China: Digital Yuan (e-CNY)

China is the farthest along. The digital yuan has been in development since 2014 and is now being tested in dozens of cities with millions of users. It’s available through mobile apps, and citizens can use it for payments at millions of merchants. The digital yuan is not fully anonymous—transactions are traceable, which aligns with China’s focus on financial surveillance.

European Union: Digital Euro

The European Central Bank is in the investigation phase for a digital euro, with a decision on whether to proceed expected around 2025. The digital euro would complement cash, not replace it. Privacy is a major concern, with the ECB stating it would not have access to personal data.

United States: Digital Dollar

The US is moving more slowly. The Federal Reserve has published discussion papers and conducted research but has made no decision to proceed. Political debates around privacy and the role of the private sector are intense. A digital dollar could take years, if it happens at all.

Other Notable Projects

- Sweden: e-Krona – Testing since 2020 as cash usage plummets.

- Bahamas: Sand Dollar – Launched in 2020, the world’s first retail CBDC.

- Nigeria: e-Naira – Launched in 2021, though adoption has been slow.

- India: Digital Rupee – Pilot programs launched in 2022.

- Jamaica: JAM-DEX – Launched in 2022.

- Eastern Caribbean: DCash – Eight countries using a shared CBDC.

Potential Benefits of CBDCs

For Citizens

- Access to risk-free digital money: Like cash, but digital. Not dependent on bank solvency.

- Financial inclusion: Anyone with a phone could have a CBDC wallet, even without a bank account.

- Potentially lower costs: No interchange fees like credit cards.

- Offline payments: Some CBDCs could work without internet.

For Governments

- Monetary policy tools: New ways to implement policy (e.g., “helicopter money” directly to citizens).

- Reduced tax evasion: Traceable transactions could make tax collection easier.

- Combat illicit finance: Less anonymous than cash.

- International competitiveness: Maintaining the role of the national currency globally.

Risks and Concerns

CBDCs also raise serious concerns:

1. Privacy and Surveillance

This is the biggest concern. If all transactions go through the central bank, the government could see everything you buy. While some designs promise tiered anonymity (small transactions private, large ones traceable), critics worry about mission creep—what starts as privacy-respecting could become a surveillance tool.

2. Banking System Disintermediation

If CBDCs are too attractive, people might move money out of commercial banks and into CBDC wallets. This would reduce banks’ ability to lend, potentially destabilizing the financial system. Central banks may address this by limiting how much CBDC individuals can hold.

3. Programmable Money Concerns

The idea of money that can be programmed to expire or restrict what you buy raises fundamental questions about freedom. Would the government limit what you can purchase? Could they freeze your funds without due process?

4. Technical and Security Risks

A centralized digital currency system would be a huge target for hackers. A successful attack could destabilize the entire financial system.

5. International Implications

If China’s digital yuan becomes widely used internationally, it could challenge the US dollar’s dominance. This has geopolitical implications.

CBDCs vs. Stablecoins

Stablecoins like USDT and USDC are private-sector digital currencies pegged to fiat. They’re already widely used in crypto. CBDCs are the public-sector response:

| Aspect | Stablecoins | CBDCs |

|---|---|---|

| Issuer | Private companies (Tether, Circle, etc.) | Central banks |

| Backing | Reserves (cash, treasuries, commercial paper) | Full faith and credit of the government |

| Regulation | Evolving, often unclear | Directly regulated by central bank |

| Availability | Global, permissionless (in theory) | Likely restricted to residents/citizens |

Some see stablecoins as a temporary phenomenon that CBDCs will eventually replace. Others argue stablecoins will continue to exist, serving different use cases.

The Future of CBDCs

CBDCs are coming, but slowly. The technology is complex, the design choices are fraught with trade-offs, and the political and social implications are enormous.

Key trends to watch:

- Privacy debates: How much anonymity will citizens have? This will be a major political battleground.

- International interoperability: Can different countries’ CBDCs work together for cross-border payments?

- Timeline: Most major economies are still years away from launching retail CBDCs.

- Cash coexistence: Will CBDCs replace cash or complement it? Most central banks say they’ll maintain cash alongside digital currencies.

Conclusion

Central Bank Digital Currencies represent a potential revolution in how money works. They would bring the convenience of digital payments together with the safety of central bank money. But they also raise profound questions about privacy, freedom, and the role of government in our financial lives.

For crypto enthusiasts, CBDCs are often seen as the opposite of everything cryptocurrencies stand for—centralized, controllable, and surveilled. But they’re also a recognition that digital money is the future. The question is not whether we’ll have digital currency, but who will control it.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. CBDC developments are rapidly evolving. Always consult official sources for current information.