You’ve heard the term “blockchain” thrown around in discussions about Bitcoin, Ethereum, and cryptocurrencies. But blockchain technology is much bigger than just digital money. It’s a revolutionary invention that has been compared to the internet itself in terms of its potential to disrupt industries. At its core, blockchain is a new way of storing and sharing information. This guide will break down what blockchain is, how it works, and why it matters, using simple, non-technical language.

The Problem: Trust in a Digital World

For centuries, we’ve relied on intermediaries to establish trust. When you send money to a friend, you trust the bank to deduct from your account and credit theirs. When you buy a house, you trust a government registry to record that you own it. When you sign a contract, you trust a lawyer to enforce it. These intermediaries—banks, governments, corporations—act as central authorities that we all must trust.

This system has worked, but it has weaknesses:

- Centralization: If the central authority is hacked, corrupted, or goes out of business, the entire system fails (a single point of failure).

- Inefficiency: Intermediaries take time and charge fees for their services.

- Lack of Transparency: These centralized ledgers are often hidden from public view. You have to trust that the bank hasn’t made a mistake or manipulated your balance.

Blockchain offers an alternative: a system where trust is established not by a person or institution, but by mathematics, code, and the collective power of a network.

The Simple Analogy: A Shared Google Doc

The most common and effective way to understand blockchain is to compare it to a shared Google Document.

When you create a Google Doc and share it with others, you aren’t sending copies back and forth. Everyone is looking at the same document simultaneously. Any change made is visible to all participants in real-time. There’s no central “master copy” that someone controls and others have to request access to. The document is distributed.

A blockchain is similar. It’s a shared, digital ledger (like the Google Doc) that exists across a network of computers. When someone adds a new piece of information (a “transaction”), it’s recorded on that shared ledger. Because the ledger is distributed across thousands of computers, no single person owns it, no single person can control it, and no single person can secretly change past records.

The key difference? A Google Doc can be edited by anyone with access. A blockchain has strict rules about how information is added, making it secure and immutable.

How Does a Blockchain Work? The Building Blocks

Let’s break down the components of a blockchain, using Bitcoin’s blockchain as the classic example.

1. Blocks: Containers of Data

Think of a blockchain as a digital notebook. Each page in the notebook is a block. Each block contains a list of recent transactions (or any other type of data). For example, a block might contain: “Alice sent 1 BTC to Bob,” “Charlie sent 0.5 BTC to David,” and so on.

Each block also contains some crucial metadata:

- Timestamp: When the block was created.

- A unique “fingerprint” (hash) of the current block.

- The “fingerprint” (hash) of the previous block. This is the “chain” part.

2. The Chain: Linking Blocks Together

Every block contains the hash of the block that came before it. This creates a chain. Imagine writing in a notebook where each new page not only has its own page number but also the page number of the previous page, written in invisible ink that can’t be erased. If someone tries to tear out a page or change information on an old page, the page numbers won’t match up anymore.

This linking is what makes the blockchain secure. If a hacker tries to alter a transaction in an old block, that block’s hash will change. Because the next block in the chain contains the old hash, it will no longer be valid. The hacker would then have to re-calculate the hash for that block and every single block that came after it, which requires an impossible amount of computing power.

3. Nodes: The Keepers of the Ledger

The blockchain isn’t stored in one place. It’s stored on a network of computers called nodes. Every node has a complete copy of the entire blockchain. When a new block is created, it’s broadcast to all the nodes. Each node independently verifies that the block follows the rules (e.g., that Alice actually had 1 BTC to send). If a majority of nodes agree the block is valid, it’s added to their individual copies of the ledger.

Because thousands of nodes each have a copy, the system is incredibly resilient. Even if one node goes offline or is hacked, thousands of other copies exist. This is decentralization in action.

4. Consensus Mechanisms: Agreeing on the Truth

How do all these independent nodes agree on what the “official” blockchain looks like? This is achieved through a consensus mechanism. It’s a set of rules that allows a decentralized network to agree on a single source of truth without a central leader.

The two most common are:

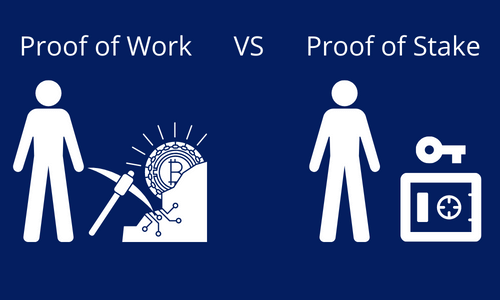

- Proof-of-Work (PoW): Used by Bitcoin. Nodes called “miners” compete to solve a complex mathematical puzzle. The first one to solve it gets to add the next block and is rewarded. This “work” requires massive energy, making it prohibitively expensive to attack the network.

- Proof-of-Stake (PoS): Used by Ethereum (after “The Merge”) and many others. Instead of miners, there are “validators” who lock up (stake) their own coins as collateral. The network randomly chooses a validator to add the next block. If they act dishonestly, they lose their staked coins. This is much more energy-efficient.

Key Properties of Blockchain Technology

Now that we know how it works, let’s look at the properties that make blockchain revolutionary:

- Decentralization: No single entity controls the network. It’s managed by a global community of participants. This removes the single point of failure.

- Immutability: Once data is recorded on a blockchain, it is extremely difficult to change or delete it. The cryptographic linking of blocks ensures the integrity of the entire history.

- Transparency: On public blockchains like Bitcoin and Ethereum, anyone can view the entire transaction history. This creates unprecedented accountability.

- Security: The combination of cryptography, decentralization, and consensus makes blockchains incredibly secure against hacking and fraud. An attacker would need to control a majority of the network’s computing power (51% attack), which is practically impossible for large networks.

Blockchain Beyond Cryptocurrency

While blockchain is the foundation of crypto, its potential applications extend far beyond digital money. Here are a few real-world use cases:

Supply Chain Management

Imagine being able to scan a QR code on a product and see its entire journey from raw material to store shelf. Blockchain can create an immutable record of a product’s origin, location, and handling. This helps verify authenticity (fighting counterfeits), ensure ethical sourcing, and improve efficiency. Companies like IBM and Walmart are already using blockchain for food safety tracking.

Healthcare

Patient data is currently siloed in different hospital systems. Blockchain could create a secure, unified, and portable health record that patients control. They could grant access to doctors as needed, improving care coordination and data privacy.

Voting Systems

Blockchain-based voting could potentially make elections more transparent, verifiable, and secure. Each vote could be recorded as a transaction on an immutable ledger, making it nearly impossible to alter results without detection. Several pilot programs are already underway around the world.

Digital Identity

Billions of people worldwide lack official identification. Blockchain could provide a self-sovereign digital identity that isn’t controlled by any government or corporation. This would allow people to access financial services, vote, and prove who they are.

Intellectual Property and Royalties

For artists, musicians, and creators, blockchain (especially through NFTs) can prove ownership and automate royalty payments. Every time a piece of digital art is resold, a smart contract could automatically send a percentage back to the original creator.

Types of Blockchains

Not all blockchains are the same. They generally fall into three categories:

- Public (Permissionless) Blockchains: Anyone can join, read the data, and participate in the consensus process. Examples: Bitcoin, Ethereum. These are fully decentralized and transparent.

- Private (Permissioned) Blockchains: Access is restricted to a specific organization or group. The network is controlled by a central entity. These are more like traditional databases but with some blockchain features. Often used by companies for internal purposes.

- Consortium Blockchains: A hybrid model where a group of organizations (like a consortium of banks) shares control of the network. It’s decentralized among the members but not open to the public.

Common Misconceptions

- “Blockchain and Bitcoin are the same thing.” No. Bitcoin is an application that runs on blockchain technology. Blockchain is the underlying platform, like the internet, while Bitcoin is one service on it, like email.

- “Blockchain is completely anonymous.” No. Transactions on public blockchains are pseudonymous (linked to an address, not a name). With enough data analysis, transactions can often be traced back to individuals. This is why it’s called “pseudonymous,” not “anonymous.”

- “All blockchains are secure.” The security of a blockchain depends on its size and consensus mechanism. Small, new blockchains with few nodes can be vulnerable to 51% attacks.

Conclusion

Blockchain is a foundational technology with the power to reshape how we store data, establish trust, and transact in the digital age. By combining decentralization, cryptography, and consensus, it offers a new paradigm where trust is built into the system itself, not placed in a central authority. While it gained fame through cryptocurrencies, its potential applications in supply chains, healthcare, voting, and beyond are just beginning to be explored. Understanding blockchain is essential for anyone looking to grasp the future of the digital economy.

Disclaimer: This article is for informational purposes only and does not constitute financial advice.